Before the introduction of currency, we had a barter system for the exchange of goods and services in ancient India since the Vedic ages. Over the years, the barter system had been replaced by more convenient precious metals or metals of different weights for the exchange of goods. The excavations at Mahenjo-Daro present strong evidence indicating the existence of such systems in the Indus Valley civilisation. Slowly, the barter system gave way to a better system of the monetary economy through the introduction of coins for transactions and purchases – known as currency.

Over the years, the currency has taken precedence as the single system that controls all forms of transactions. According to the encyclopaedia, the currency is standardisation of money in any form, in use or circulation as a medium of exchange, for example, banknotes and coins. A more general definition is that a currency is a system of money in common use within a specific environment over time, especially for people in a nation-state. Earlier, the currencies were divided into three categories of monetary system, such as flat money, commodity money and representative money. With the advent of computers and the Internet in recent times, another form of currency is highly in use i.e. digital currency.

In India, our very own currency the “Rupee” dates to the 6th Century BCE. India alongside Lydia and China was one of the earliest issuers of coins in the world. The coins were first used in Mahajanapadas or Independent Kingdoms in ancient India including Gandhara, Kuntala, Kuru, Panchala, Shakya, Surasena, and Saurashtra out of a total of sixteen.

The term “RUPEE” is derived from the Sanskrit word “rūpya”, which means “wrought silver”, and maybe also be something stamped with an image or a coin. During the reign of Samrat Chandragupta Maurya (circa 340 to 290 BC), his Prime Minister Chanakya is known to have mentioned the minting of coins such as Rupyarupa (silver), Suvarnarupa (gold), Tamararupa (copper) and Sisarupa (lead) in his famous book titled “Arthashastra”. Over the years, from the era of Moghuls to the British, Rupee has changed many names from Rupyakam, Jittals, and Tanka to Rupiya during the reign of Sher Shah Suri.

ALSO READ: EXC: No Internet, No Worry: India’s Digital Rupee To Transact Offline

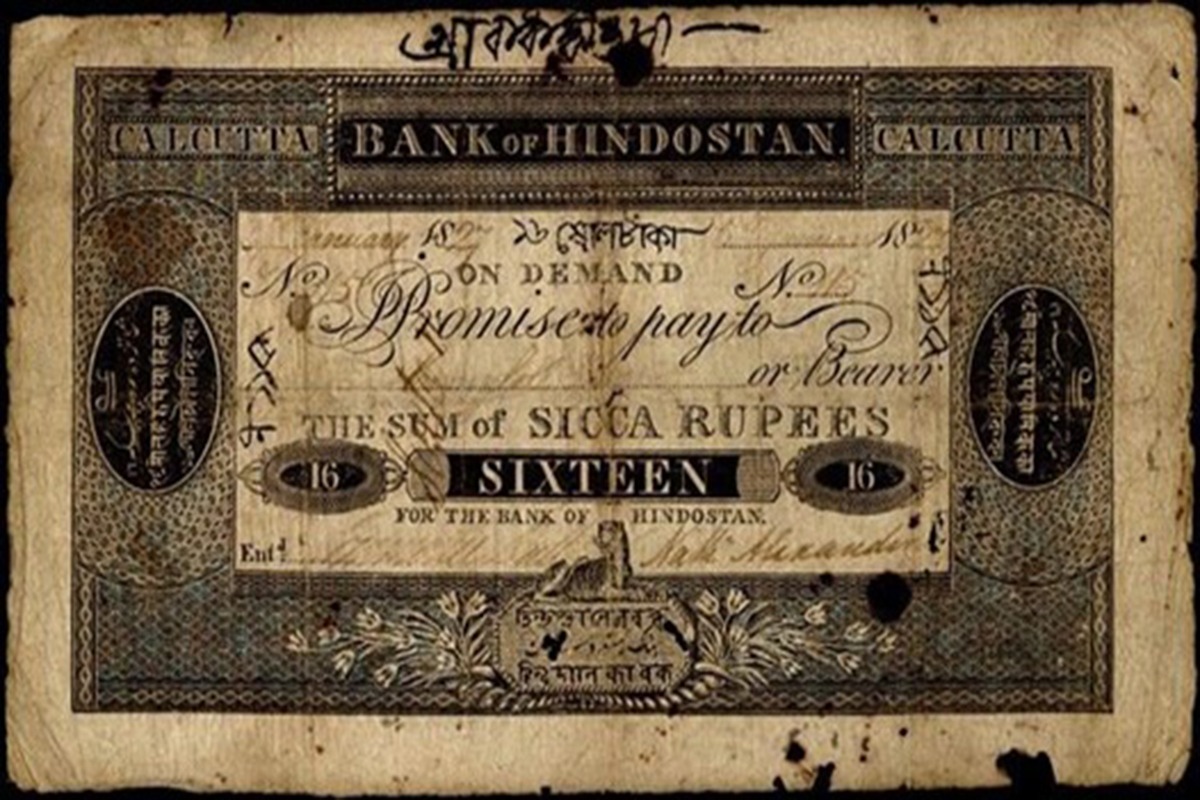

This metal Rupiya kept going on afterwards in British rule until in the 18th Century paper currencies arrived when two banks the Bank of Hindostan General Bank in Bengal and Bihar and the Bengal Bank became the first banks in India to issue paper currency.

As per the Reserve Bank of India (RBI) chronicles, the transition of currency management from colonial to independent India was a reasonably smooth affair. Midnight, August 14, 1947, heralded Indian independence from colonial rule. The Republic, however, was established on 26th January 1950. During the interregnum, the Reserve Bank continued to issue the extant notes. The Government of India brought out the new design Re 1 note in 1949. Finally, in the year 1950, the first Republic India banknotes were issued with denominations of Rs 2, 5, 10 and 100 having slight variations in colour and design.

Over the years, we have seen many forms of Indian currencies ranging from 500, 1000 to 2000 rupee notes after demonetization. Also, many coins of Rs 5 and 10 value were minted during the journey, until recently. On 6th June 2022, Prime Minister Narendra Modi launched a special series of Re 1 and Rs 2, 5, 10 and 20 denomination coins on the occasion of Azadi Ka Amrit Mahotsav, which are also ‘visually impaired friendly’. These coins have the ‘Azadi Ka Amrit Mahotsav’ (AKAM) design.

With the exponential growth of technology and the Internet, there is an increased use of digital currency including plastic money called ATM/debit/credit cards. Off late, another form of currency known as cryptocurrency – an alternative form of payment created using encryption algorithms – is in use for the purchase of certain goods and services in some countries. But there is huge scepticism about cryptocurrencies as they can be misused for money laundering, tax invasion and terror financing.

The more legitimate and alternate form of digital currency is the Central Bank Digital Currency (CBDC) launched by various central banks across the world. A CBDC is a high-security digital instrument like paper banknotes and is a means of payment, a unit of account, and a store of value. Like paper currency, each CBDC unit is uniquely identifiable to prevent counterfeiting. Its normally issued by the central bank of a sovereign nation and is freely convertible against the physical currency issued by the same central bank. A customer or user does not need to have a bank account for doing transactions using CBDCs.

According to a study by the Atlantic Council Geo-economics Centre, it is found that around 105 countries are considering launching their own CBDC that would be primarily used for interbank transactions, including most of the G20 countries.

During the Union Budget 2022, Union Finance Minister Nirmala Sitharaman asked the public to exercise caution while dealing in cryptocurrencies, saying that CBDCs will be fully launched in India by 2023. She had also said that the Indian CBDCs would be safe and incur lesser transaction costs. Considering the evils associated with it, the Modi government imposed heavy taxes on cryptocurrency and virtual digital assets to control their rising misuse for illegal activities.

In line with the global CBDC plan, on 1st November 2022, the RBI launched the e-Rupee, which will have two types of usage: Retail CBDC (e₹-R) and Wholesale CBDC (e₹-W). While e₹-R will potentially be available for everyone i.e. the public, e₹-W is designed for restricted access to select financial institutions and will be used for interbank settlements plus other wholesale transactions.

While with UPI transactions, any transfer on the platform might seem instantaneous but the settlement happens on the backend between two banks and takes some time; but with CBDC or e-Rupee, the programmable nature of money will allow the user to make settlements instantly. Apart from reducing the transaction cost, it will enable the government to control the money flow in and out of the country or hawala transactions. Since it can’t be burned, destroyed or even physically lost, it’s more durable than paper currency. It is also expected to make interbank transactions efficient, and more importantly, it will help reduce our dependence on US Dollar.

Like every other new project or plan has its pros and cons, the e-Rupee can’t be left without its merits and demerits. Since then it is an introductory pilot project, it is too early to say anything about its effectiveness. However, the concerns regarding cyber security and data privacy remain – particularly if the user data falls into wrong hands.

Some critics are of the opinion that India has taken a hasty decision in launching the e-Rupee and will face issues just like the situations that arose after the demonetization. But the Narendra Modi government has maintained that India will no longer wait for developed countries to make the first move but instead leverage its technological prowess to strengthen its economy and national security.

(Prabin Kumar Padhy is an entrepreneur and management consultant.)

Disclaimer: Views expressed above are the author’s own.